Circular Economy Innovations in Chemicals, Water & Waste

While significant strides towards decarbonization have been achieved, carbon is here to stay. Carbon is an essential part of our lives and we are going to continue to need it, However, usage needs to be guided by circular economy principles which maximize resource efficiency – including in recycling applications. Further, in a water-scarce world with ever-changing pollutants and increasingly stringent regulations, traditional water treatment systems are no longer fit for purpose. Innovation and investment across these challenging sectors will continue to drive new market opportunities and essential changes to the status quo.

Examples such as Climeworks, developer of atmospheric carbon removal, which raised $76 million to build a CO2 to fuel plant will continue to emerge. The time is now for the circular market.

CO2 to Chemicals

The CO2 to chemicals landscape includes both bio-based technologies as well as alternatives such as electrochemical (and others). CO2 utilization pathways such as for cement, mineralization aggregates, proteins, is not sufficient for the potential volume of captured CO2. As such, chemicals (and fuels) can provide alternative utilization pathways for large amounts of CO2.

Many utilization solutions face challenges around cost and ultimately, there needs to be policy mechanisms in place which help to address the cost of CO2 in the atmosphere. Recently, big tech has become increasingly involved in carbon removal or reduction technologies, either through investment or offset purchase through companies like CarbonCure. This may help address the green premium, in the cases where policy is not sufficient.

Chemical products can include: Ethylene, Methanol, CO/Syngas, Formic acid, Lactic acid and Polyols.

Recent investment examples include:

- November 2020: Total, L’Oréal have premiered sustainable packaging made from captured and recycled carbon emissions with Lanzatech. LanzaTech captures industrial carbon emissions and converts them into ethanol. Total converts the ethanol into ethylene before polymerizing it into polyethylene which is used by L'Oreal.

- October 2020: Mitsubishi Power and consortium of organizations will collaborate on the North-C-Methanol large-scale demo plant. The plant will convert green hydrogen and captured CO2 emissions of local industrial partners such as ArcelorMittal, Alco Bio Fuel and Yara into 44,000 tons of green methanol annually.

- September 2020: Evonik and Siemens commissioned a pilot plant for CO2 to Chemicals. The project is sponsored by BMBF for €6.3 million ($7.4 million) as part of the Rheticus project.

Even as the market moves away from fossil fuels as feedstock there will still be demand for carbon. Alternative sources such as biomass and waste (e.g. plastic waste) will not provide sufficient volume of carbon. Production with CO2 vs chemicals uses less land.

Although interest in Direct Air Capture Carbon continues to increase, industrial emissions remain a relatively low-cost source of carbon in comparison. Technologies, like those demonstrated by Svante enable the capture much of this at decreasing costs. One of the near-term challenges remains the market pull for CO2 utilization yet technologies like Synhelion’s show that there are effective solutions for industrial emitters and consumers such as the aviation industry.

Water Treatment & Harvesting

Cleantech wastewater treatment, reuse and water harvesting technologies are becoming smarter, cheaper, and more efficient while the commercial and industrial market is becoming more open to innovation.

Due to Covid-19, increasing consumer concern for health and lack of trust for municipal water treatment investment in Q4 2020 focused on B2C solutions for efficiency and health. Orbital Systems closed its first Growth Equity round raising $23.8 million. Healthy drinking water provider Oxigen raised $15 million in a Series A round. Q1 and Q2 2020 saw a similar trend with a focus on water security with investments into waster harvesting technologies. SOURCE, developer of solar-powered atmospheric water harvesting systems, raised $50 million. THE.WAVE.TALK, developer of IoT sensor to monitor micro-organisms in water, raised $2 million. LARQ, developer of self-cleaning water bottles raised $6.3 million.

Commercial and industrial manufacturers are increasingly investing in water technologies. In December 2020 Alcoholic drinks manufacturer Diageo launched Diageo’s Sustainable Solutions, a global platform that will provide non-equity funding to innovators. This included a search for water stress mitigation technologies. Similarly, drinks company ABinBev launched its second cohort for its 100+ Sustainability Accelerator which has included 7 water saving innovators to date including Desolenator, developer of a family sized solar powered water desalination and purification devices and Gybe, provider of water data on sediment flows, excess nutrients and algal blooms in waterways using satellite data.

Water innovation in Switzerland has followed similar investment trends with a focus on water saving technologies. In October 2020, Droople, developer of IoT platform which creates a smart grid for commercial and industrial water use, won $92,900 grant from Switzerland Innovation. In March 2020, Hades AI, developer of AI software to identify cracks, leaks and blockages in water infrastructure, was selected to join the URBAN-X Accelerator Program receiving $150,000 in seed funding (see table 1 below).

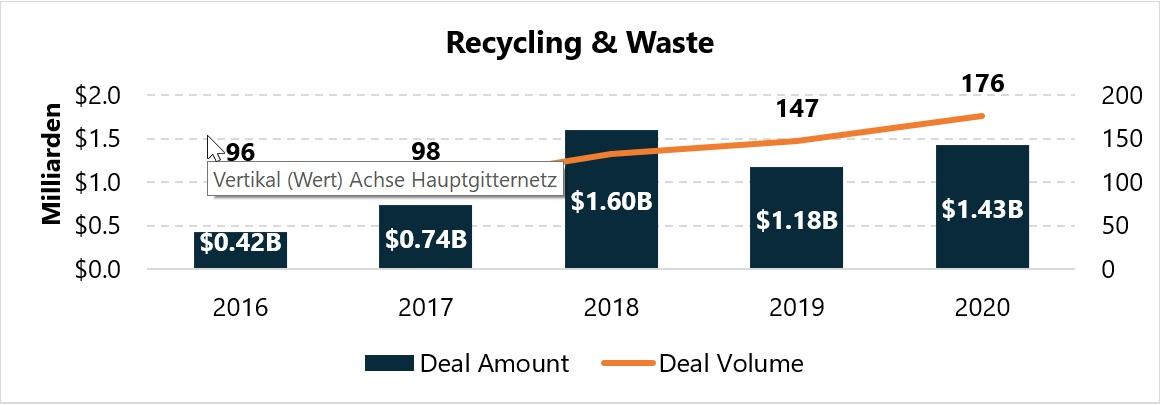

Waste Investments Soar

The last few years have been transformational for the cleantech waste sector, Cleantech Group have recorded record investment in 2020 reaching $1.43 billion, the number of innovators has also blossomed at 176. This is due to four key drivers:

- Consumer awareness of the impact of plastics on our environment has created a market for reuse, refill and decomposable consumer products and business models.

- Waste export bans across the globe, starting with China’s National Sword Policy in 2018, have diminished the export market forcing export countries to invest in domestic waste infrastructure.

- In response to consumer and industry pressure Fast Moving Consumer Goods (FMCG) companies and plastic producers are pursuing consumer focused recycling strategies and collaborating to develop chemical plastic recycling infrastructure.

- Regulation is shifting the responsibility of funding waste infrastructure onto producers via plastics taxes and other Extended Producer Responsibility (EPR) regulations.

Consumer demand for plastic free consumer products is encouraging investment in innovators with circular business models. In December 2020, provider of reusable packaging logistics services, Loop raised $25 million in a Series A round with strategic investors Nestle, Suez and Proctor & Gamble. That same month, Unicorn e-commerce retailer for sustainable home essentials Grove Collaborative raised $125 million in a Growth Equity round.

In 2020 Q4 saw continued investment and corporate activity into plastics recycling Plastic Energy partnered with Total, Nestle and Renewi to develop separate chemical recycling facilities in the UK, France, and Netherlands, respectively. Plastic Energy also partnered with UK Supermarket, Tesco to trail closed-loop pyrolysis recycling; and with SAP’s, GreenToken to develop a plastic-tracking blockchain system. In October 2020, the UKRI announced an $27.3 million in public and private project finance for cutting edge plastic recycling plants, funding projects by ReNew, Recycling Technologies, Poseidon Plastics and Veolia (see table 2 below).

Switzerland Recycles, but there is work to do

Switzerland has achieved a recycling rate of over 50% however, the country is one of the highest waste producers per capita in Europe. The last 12 months there has seen investment and acquisitions into plastics recycling and utilization business models. Sion based developer of chemical recycling technology for PET, Depoly won the MassChallenge Switzerland 2020 in October 2020 winning $71,000 in grant funding. In December Depoly raised $1.4 million in seed funding to develop a recycling pre-demo plant for the depolymerization of PET plastic to the raw materials required to produce PET plastic. In February 2020, Zurich based plastic recycler, Minger was acquired by Mitsubishi Chemical Advanced Materials (MCAM) allowing MCAM to establish an integrated business model for engineering plastics, from manufacturing to sales, machining, collection, and reuse in Switzerland.